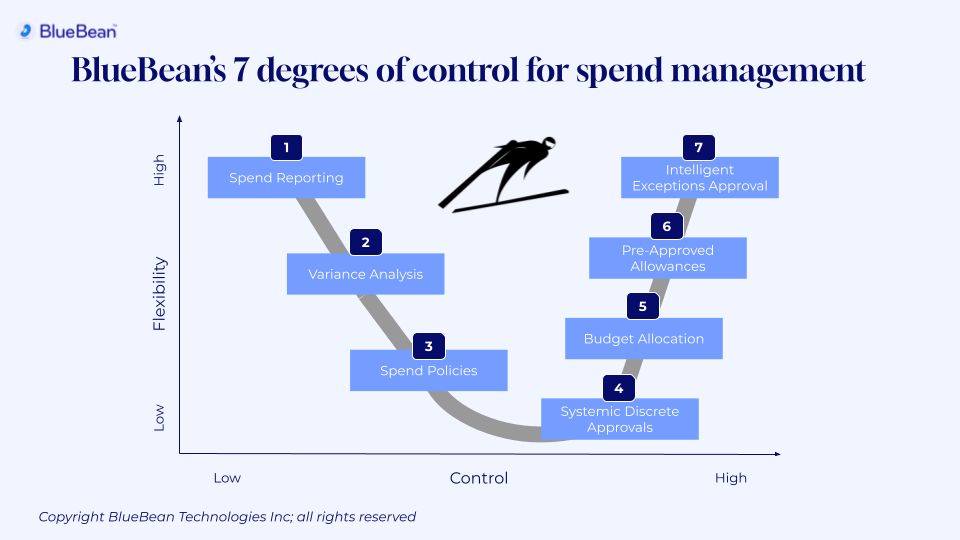

The 7 degrees of control for spend management is a comprehensive framework that articulates options companies can choose from to control their expenses. Each of the 7 approaches introduced in the framework offers a desired degree of control for a certain level of flexibility.

The first four approaches see a progressive increase in control at the expense of flexibility to eventually witness a sharp upturn in flexibility while expanding control with the last three. This U shape curve is largely explained by a shift from a rather passive management to a more active and segmented approach of controls.

Companies can adopt one of the seven approaches. Yet the seven degrees of control are not exclusive from each other. Used thoughtfully as a whole they can indeed provide a comprehensive set of practices to establish an ideal balance between controls and flexibility for any organization.

- Spend Reporting

- Variance Analysis

- Spend Policies

- Systemic Discrete Approvals

- Budget Allocation

- Pre-approved Allowances

- Intelligent Exceptions’ Approval

Spend reporting: spend reporting consists in organizing expenditures in a structured way with the intention to better understand where the company is spending its money. When implemented this practice allows companies to react to their expenses albeit after they occurred.

Variance analysis: relying on spend reporting as well as budgets and forecasts across multiple time periods, variance analysis is a practice that aims at explaining what drove fluctuations in spending. By understanding root causes, variance analysis allows to establish a series of actions to control spending. With a bias for action, variance analysis remains backward looking.

Spend policies: spend policies establish a series of guidance for employees to follow when engaging the company’s money. More forward looking than spend reporting and variance analysis to influence behavior before spend occurs, the practice falls however short of establishing proactive guardrails to systematically enforce policies.

Systemic discrete approvals: the practice requires that every purchase request goes through a sequence of approvals. While systematic approval is required to grant a purchase, discrete actions, groupthink behavior from sequenced approvals and the need to expedite decisions, prevent its actors to distinguish the forest from the trees leading to unintentional leakages. Flexibility disappears however controls end up not being as effective as what they may appear to be.

Budget allocation: allocating a budget consists in empowering a member of an organization with a set amount of money which they are free to spend the way they see fit to achieve a desired outcome. This practice provides flexibility and delegates controls of a pre-approved amount of money to the organization’s leaders. Controls are in place and flexibility within the organization returns.

Pre-approved allowances: similarly to budget allocation, pre-approved allowances add a policy element to establish guidance by category or type of spending. The practice enables the harmonization of rules within the organization through safeguards. While increasing control, budget leaders maintain complete freedom of allocation. Approvals are only required if purchase requests fall outside the set guidance.

Intelligent exceptions approval: intelligent exceptions approval is the equivalent of a pre-approved allowance practice which would account for market fluctuations as they occur instead of set values. Introducing market dynamics creates additional flexibility without compromising controls. Similarly to pre-approved allowance, approvals are only required if purchase requests fall outside the guidance now linked to market benchmarks.