Meet BlueBean

TM

We Digitize your Corporate Card Program so you save time and earn more on online and in-store purchases of any size.

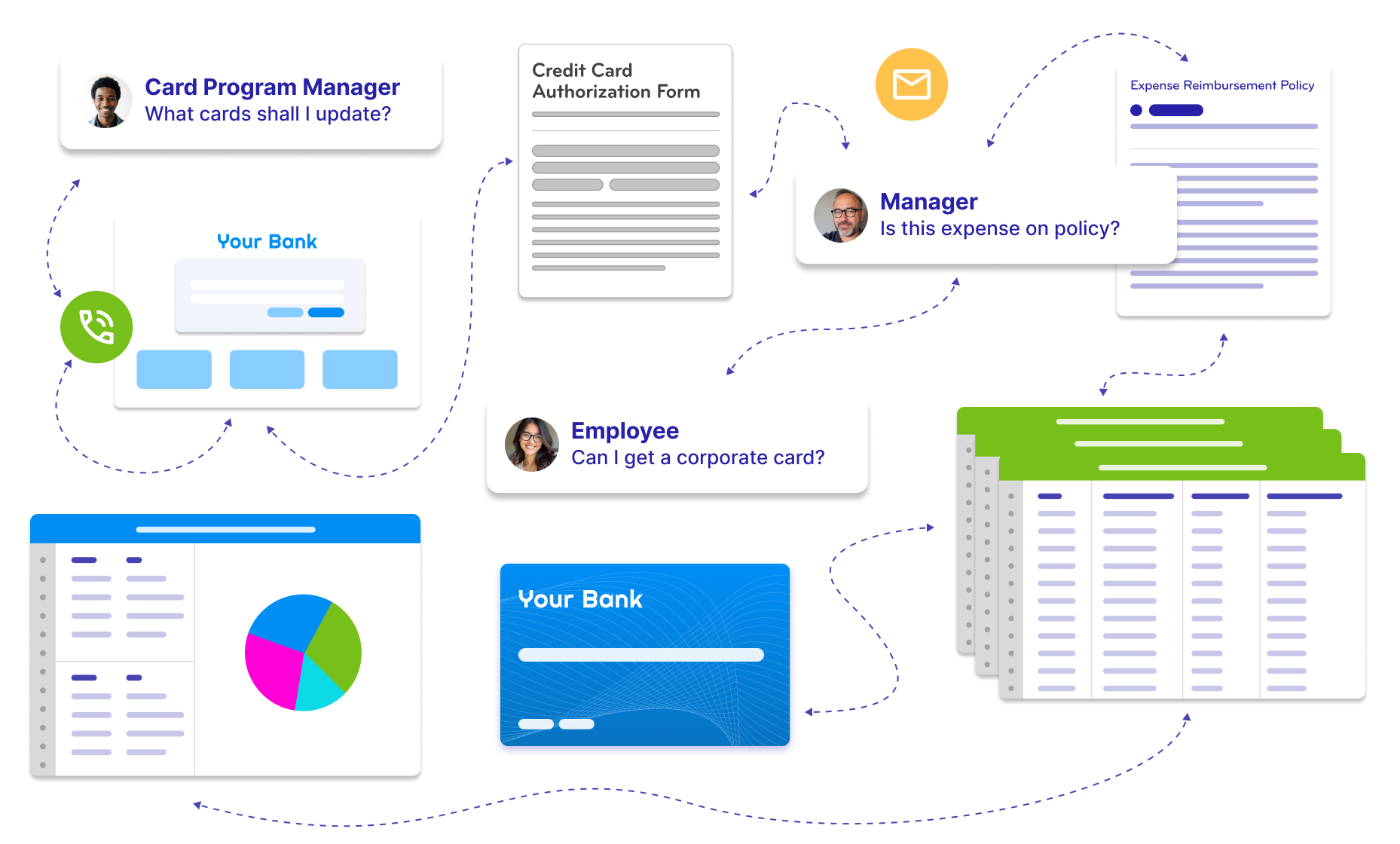

Corporate Card Programs Were Built for Another Era

Most organizations still manage physical card programs manually through forms, bank portals, expense systems and spreadsheets.

The result is slow onboarding, weak visibility, delayed reconciliation and unnecessary processing costs.

BlueBean Digitizes the Entire Card Experience

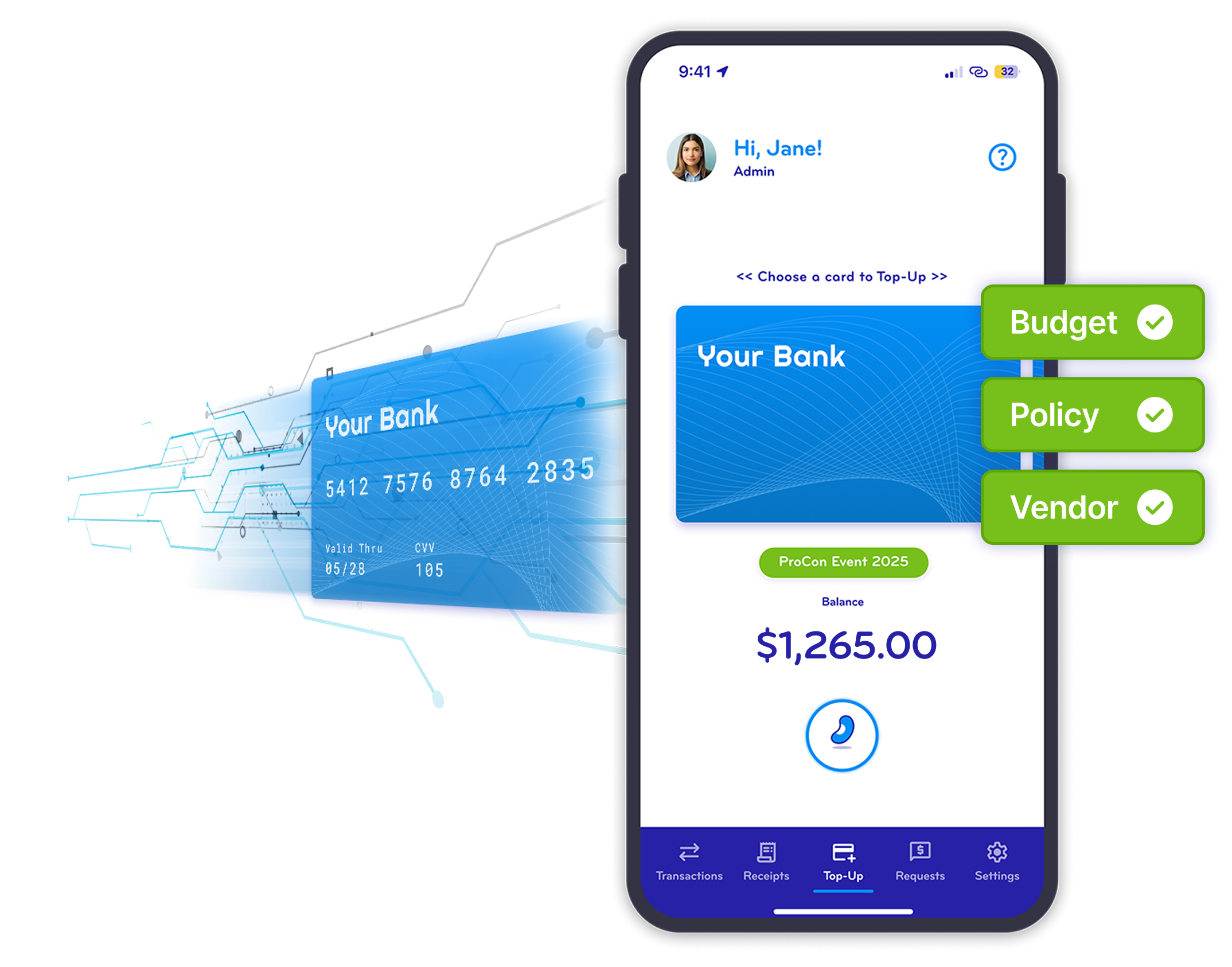

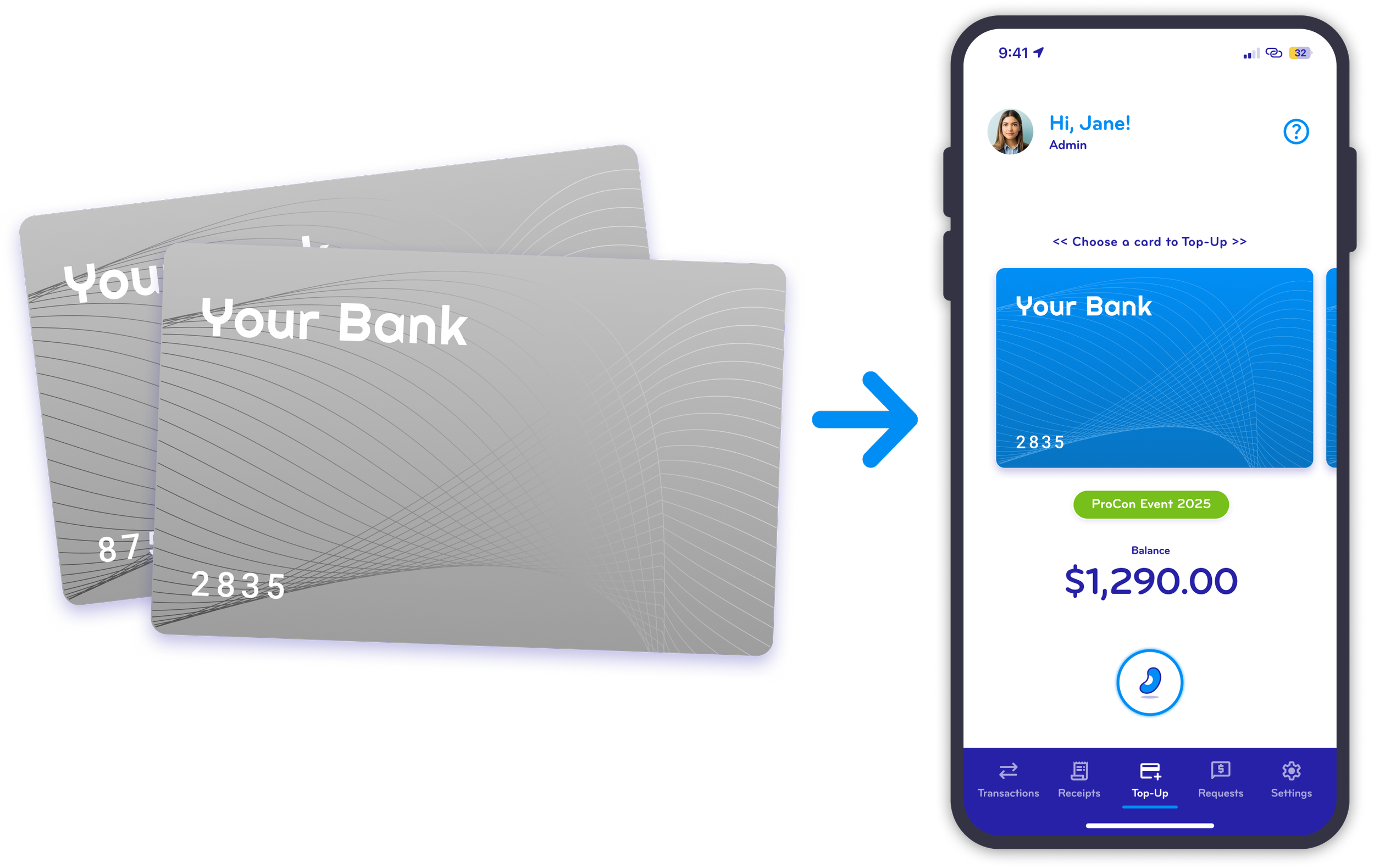

Instant Card Issuance

Issue single-use or multi-use virtual cards instantly on-demand with built-in approval workflows and controls.

Automated Expense Reconciliation

Capture receipts and transaction data in real time at authorization instead of days later and automate reconciliation.

Pre and Post Purchase AI Powered Controls

Add automated supplier, budget and policy controls before and after purchases happen.

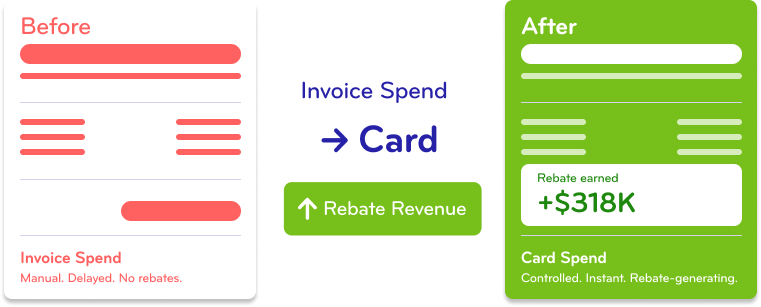

Move Beyond Small Purchases

Traditional card programs restrict card usage to low-value transactions because controls are often limited to spend limits and MCC restrictions, leaving compliance and validation to manual reviewers after payment has already occurred.

BlueBean changes that.

With AI-powered controls and configurable approval workflows applied before cards are issued, organizations can confidently use cards for significantly larger purchases directly at supplier checkout.

That means:

More spend on card

Fewer invoices

Faster supplier payment

Greater rebates

Lower processing costs

Recognized by Leading Voices in Procurement

Higher Control. Lower Cost. Greater Value.

Lower Processing Costs

Reduce invoice and reconciliation workload by shifting purchases to cards.

Increased Rebates

Expand card usage to larger purchases and maximize bank rebate generation.

Reduced Software Costs

Decrease dependency on P2P and invoice processing tools for online purchases.

Learn how to use BlueBean

(in about a minute)

Setting up BlueBean is as easy as 1 - 2 - Click!

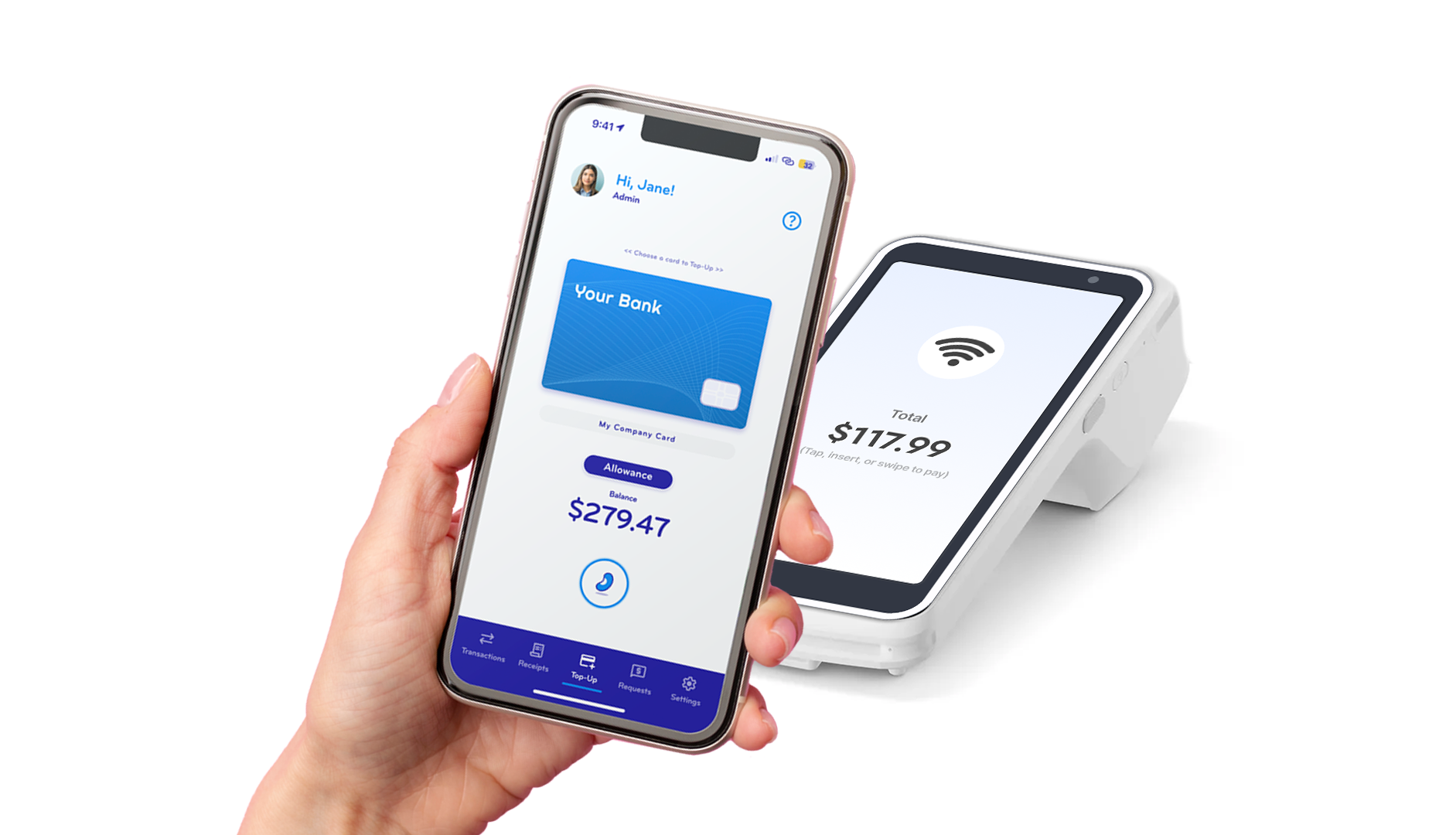

Connect your eligible business or corporate card account.

Set up your controls and invite your employees.

Click to pay with complete control at every online check out.

Any questions?

The Physical Corporate Card Is Becoming Obsolete

A new generation of employees expects payments to be:

Digital

Instant

Mobile

Embedded

Invisible

BlueBean helps organizations modernize commercial payments without replacing their existing banking relationships.

Built to work with your existing card program across all three major card networks

BlueBean is not a bank. BlueBean overlays existing commercial card programs to simplify operations and modernize user experience while preserving banking relationships.

Join the Companies Turning Spend Into Savings with BlueBean

Companies of all sizes use BlueBean to control spending, automate accounting, and earn rebates on every dollar spent.

Chris Skinner

VP Research & Development, Cognitus

“We use BlueBean to make employee expenditures easier to manage. When someone needs to book a flight or buy office supplies, BlueBean not only gives them access to a virtual card to make the purchase, but automatically captures the receipt and related information, saving them the time and hassle of submitting an expense report.“

Teagan Clare

Lab. Technician, Safety Officer, ExocelBio

“With BlueBean, getting virtual cards approved at check out and capturing receipts for buying lab supplies is so simple. The auto-approval keeps spending in check and manual approval is only needed for exception purchases. By using their marketplace we were able to save 10% from what we used to pay.”

Eric George

Co-Founder and CEO, Blu Buying Club

“I was blown away by the Blue Bean extension. It only took 10 minutes to learn, and it is incredibly easy to use. The BlueBean solution has streamlined vendor management and simplified payments and accounting. It's intuitive and saves us valuable time, allowing us to focus on business growth and automate back office tasks.”